Costs (31.2), Part II

- Thiago Casarin Lucenti

- Feb 13

- 2 min read

Chapter 32 - Costs

Lesson Objective: To understand the basic concepts of costs before learning costing techniques

What are the reasons cost data/information is so important for businesses?

Why should managers have accurate cost data?

Cost data is important for various reasons:

Costs aid on pricing decisions;

Costs are also important for production decisions:

Whether to stop the production of a product;

Whether to increase production;

Whether to implement new methods;

Whether to choose different materials.

Cost is an important measure for comparison:

Comparing different periods;

Comparing with set targets.

We will learn two different costing techniques on this chapter but before going into them we need to clarify some concepts:

Overhead costs are the costs of running a business such as rent, insurance, utilities, etc. They cannot be avoided but should be reviewed frequently to increase profitability. Overheads can be divided into four:

1. Production/Manufacturing Overheads:

2. Selling and Distribution Overheads:

3. Administrative Overheads:

4. Finance Overhead (Interest and Loans)

Other important concepts before costing techniques include:

Unit Cost - The average cost of producing each unit of output

Cost Centers:

Profit Centers - an identifiable part of the business for which is possible to identify revenues and costs and therefore calculate profit (e.g. individual shops in a retail chain, local branches, geographical region, a team or individual responsible for sales):

Businesses make this division (cost and profit centers) for some obvious reasons:

So that targets for managers and workers can be set;

So that performance can be assessed;

So that areas for improvement can be identified;

To aid decision making.

The problems of dividing centers, on the other hand, are:

May create unhealthy competition between centers (loss of organizational purpose/direction);

Inaccuracies as some indirect and overheads costs cannot be allocated to specific centers;

External influences in different centers are not taking into account.

We will soon learn two separate costing techniques:

Full-Costing Technique (a.k.a. Absorption Costing);

Contribution Cost (a.k.a. Marginal Costing).

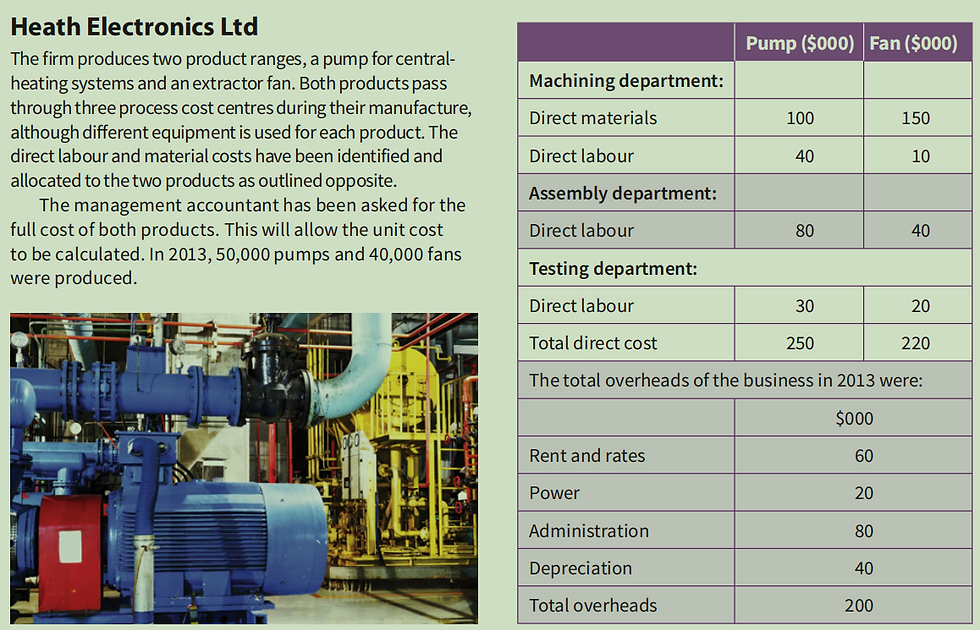

The major problem with costing methods relates to cost allocation:

Allocating direct labor and direct materials to an individual product is easy...

Overheads and indirect costs, however, are hard to individually allocate making it hard to properly answer the question:

"How much does it actually cost to produce this product?'

To-Do-List:

Chapter 32 - Costs

Comments